I signed up for a free trial, set a calendar reminder, then blinked and saw another charge. It happens to sharp people with full plates. The bigger question is what I can do next. Some renewals are lawful. Others cross the line when companies hide terms, skip reminders, or make canceling feel like a maze. That is where my rights kick in.

Can I sue a company for auto-renewal subscriptions?

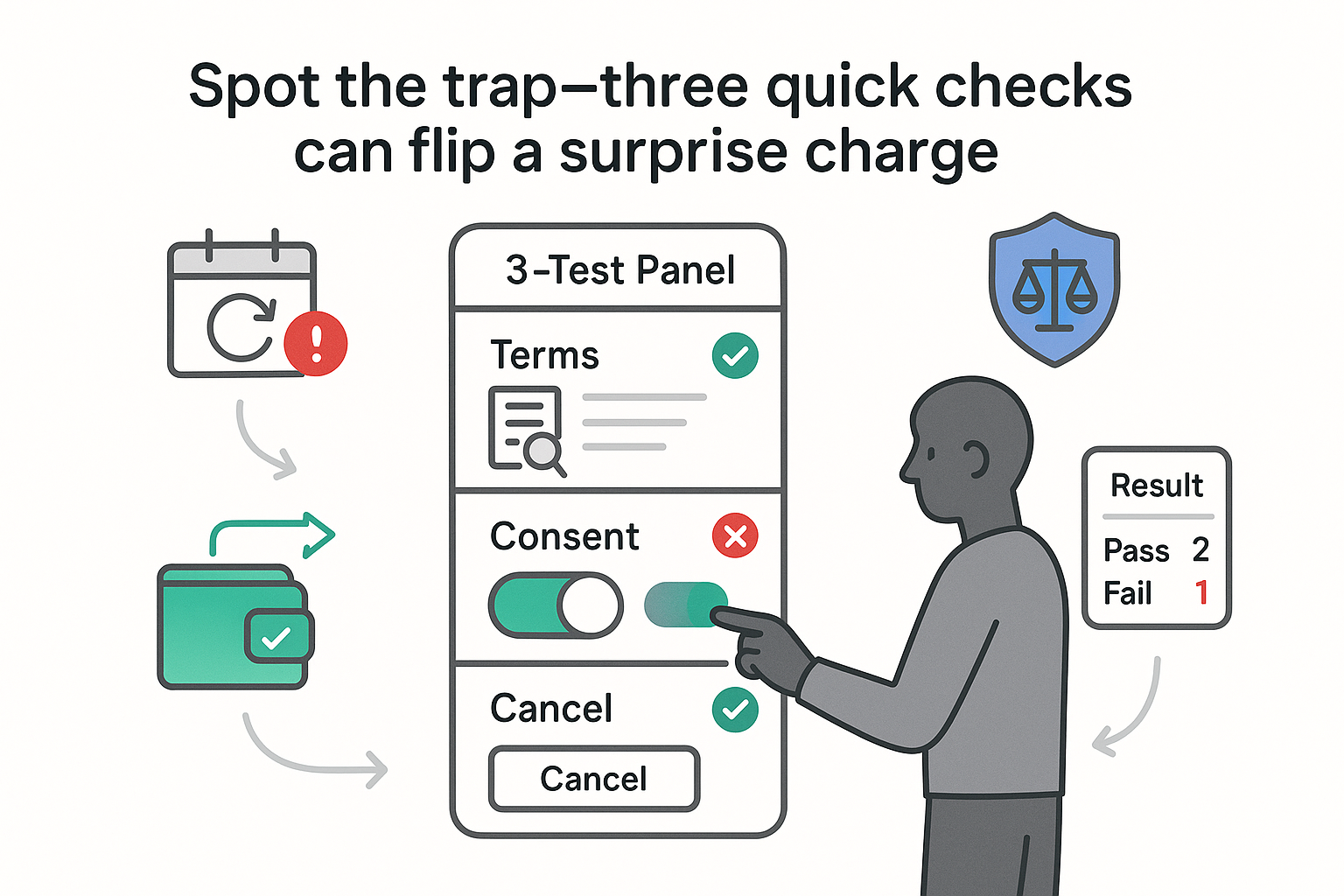

Yes - I can sue when a company violates the federal Restore Online Shoppers' Confidence Act (ROSCA) and state automatic renewal laws, or runs afoul of unfair and deceptive trade practices (UDAP) rules. The core questions are threefold: were the renewal terms clear before I paid, did I give affirmative consent, and could I cancel easily. If any of those fail, I may have a claim for refunds, statutory damages (in some states), and injunctive relief that forces practice changes.

Quick answer at a glance:

- What can qualify: hidden or unclear terms, pre-checked boxes, missing renewal reminders where required, hard-to-find or broken cancel paths, charges after I canceled.

- Likely outcomes: refunds, statutory damages in states that provide them, attorneys' fees where fee-shifting applies, and court orders that change processes.

- First moves: cancel in writing, request a refund, preserve evidence, start a chargeback if needed, then talk with counsel if the amount is large or the practice looks systemic.

This is general information based on publicly available sources. It is not legal advice. Rules vary by state and contract type, and timelines matter.

How I decide if my facts meet the test

Not every annoying renewal is illegal. Courts and regulators focus on notice, consent, and cancellation. I am on stronger footing if key facts point to a shortfall in any of these: the auto-renewal terms were buried or presented after checkout; the purchase page did not clearly show price, renewal cadence, and how to cancel; the seller used pre-checked boxes or silence as consent; the company failed to send required renewal reminders for longer terms; canceling was obstructed by forced chats, long holds, maze-like menus, or a single impractical channel; I canceled but was still charged; the account holder is a minor; or I purchased in one state while living in another, raising multi-state protections or conflicts.

If I live outside the United States, the framework changes. The UK's Competition and Markets Authority has pressed on subscription traps, and the EU has reinforced obligations around choice architecture, transparency, and simple cancellation. Cross-border subscriptions can raise jurisdiction issues I should surface early.

Evidence I capture right away

- Screenshots of the checkout flow and any pop-ups that mention terms (price, cadence, length, and cancellation).

- The terms and conditions in effect when I enrolled (I save or print to PDF; web archives can help show historical versions).

- Emails or texts confirming sign-up, reminders, and renewal notices.

- Bank or card statements showing dates, amounts, and merchant descriptors.

- Records of chats, emails, or calls about cancellation attempts, plus any cancellation confirmations.

- App or account settings that display subscription status or renewal dates.

Small detail, big impact: screenshots showing that price and cadence sat off-screen, in tiny font, or low-contrast gray can be pivotal.

The laws that usually apply

Two layers typically govern online subscriptions with auto-renewal. At the federal level, ROSCA requires three things before a charge: clear and conspicuous disclosure of key terms (price, frequency, renewal length, and how to cancel), express informed consent (no pre-checked boxes), and a simple cancellation method that is not harder than sign-up. If a company uses dark patterns to steer or trap people, the Federal Trade Commission (FTC) can also act under Section 5 of the FTC Act.

At the state level, automatic renewal laws (ARLs) and UDAP statutes add further obligations. California's Business and Professions Code §17600 et seq. requires clear pre-purchase terms, an acknowledgment email, a visible online cancel option for online sign-ups, and renewal reminders for annual plans. New York has an Automatic Renewal Law (alongside General Obligations Law §5-903 for certain service contracts) that focuses on clear terms and pre-renewal notices, especially for annual renewals. Vermont (9 V.S.A. §2454a), the District of Columbia (Automatic Renewal Protections Act), Colorado (C.R.S. §6-1-732, originating with HB21-1239), and Illinois (815 ILCS 601/ Automatic Contract Renewal Act) enforce similar themes: plain-view disclosures before purchase, affirmative consent, timely renewal notices (often 15 to 45 days before the next charge for longer terms), and an easy cancellation method that matches how I enrolled. If disclosures or cancellation channels fail, refunds or statutory penalties can follow.

Some industries (insurance, telecom, utilities) sit under separate regimes, and business-to-business agreements may be treated differently from consumer contracts. That distinction matters if I am handling a business subscription.

Unfair or deceptive design still matters

Even if a company skirts a technical disclosure rule, the broader lens is whether the overall experience misleads or is unfair. Pre-checked boxes, hidden fees, confusing countdowns or warnings that frame cancellation as risky, forced or broken cancel paths, tiny or inactive unsubscribe links, and sudden price hikes at renewal without clear notice can all trigger UDAP scrutiny under state law or Section 5 of the FTC Act. The FTC has repeatedly flagged dark patterns - see FTC Report Shows Rise in Sophisticated Dark Patterns Designed to Trick and Trap Consumers - and has brought enforcement actions against subscription traps and free trials that quietly convert.

Remedies here can include restitution to consumers, civil penalties, fee-shifting in some states, and injunctions that reshape how companies disclose, enroll, and cancel. Many states allow private actions, and class litigation is common when design impacts thousands in the same way.

What outcomes and timelines look like

If a company gets it wrong, potential consequences range from refunds (full or partial) to statutory damages where a state ARL sets fixed amounts per violation. Courts can order injunctive relief that requires clearer disclosures, real consent capture, and click-to-cancel functionality. In fee-shifting jurisdictions, the company may owe attorneys' fees and costs. Government enforcement can add civil penalties, and class actions multiply exposure when a pattern is systemic. Reputational damage often follows, which pushes churn and acquisition costs up.

Timelines vary. Individual refunds may land in weeks if a company cooperates, but chargebacks or small-claims routes can stretch into a few months. Civil litigation can run nine to eighteen months or longer, though strong documentation and practical settlement options can compress time. Whether damages scale often depends on willfulness, the number of consumers hit, prior warnings, and how quickly the company corrected course. Companies commonly argue I agreed or had notice; contemporaneous screenshots, notices, and cancellation confirmations can move the conversation.

How I dispute an auto-renewal charge

- Cancel right away and capture proof. I use the same channel I used to sign up when possible. If there is an account portal, I click the cancel button and screenshot each step and the final confirmation with a timestamp.

- Ask for a refund in writing. I include the charge date and amount, and state why the renewal was noncompliant (missing disclosure, lack of consent, obstructed cancellation). I keep it factual and polite.

- Start a chargeback if the seller will not fix it. For credit cards, the Fair Credit Billing Act gives me 60 days from the statement date to dispute a billing error with my issuer (implemented by Regulation Z). For debit cards or bank transfers, Regulation E may apply. Card networks often allow up to 120 days for services that renew, sometimes longer - issuer rules control, so I act fast.

- Document everything. I save emails, chat logs, call notes, screenshots, and a simple timeline with dates, names, and outcomes. That package makes my case easy for an issuer, regulator, or court to review.

- Report systemic issues. If the pattern looks widespread, I file complaints with the FTC and my state Attorney General or local consumer protection office. For mobile-app subscriptions, I also use the platform account portals to request refunds and flag sellers who ignore cancellation.

Detailed documentation and clear legal framing often prompt prompt refunds or credits.

When I consider legal counsel

If my issuer reverses a small, isolated charge, I may not need a lawyer. I consider counsel when the seller refuses to refund despite clear errors or proof of cancellation, the dollar amount is significant (especially with annual plans renewed without compliant notice), the design looks like it harms many consumers (potential class exposure), or my business account has repeat charges and material losses. A lawyer will evaluate my documents against ROSCA, state ARLs, and UDAP, send a demand that lays out facts and violations, negotiate refunds or broader relief (including injunctive terms), and, if needed, file suit individually or explore class relief. Some cases proceed on contingency where statutes allow fee-shifting; others use hourly or flat fees (for example, for a demand letter). Strong documentation usually shortens the timeline and raises the likelihood of resolution.

Where I read the rules or file complaints

- Federal: FTC resources on ROSCA, negative-option marketing, and dark patterns; FTC Complaint Assistant for reporting subscription traps. For background, see the FTC's Report on Dark Patterns.

- States: My state Attorney General's automatic renewal or subscription guidance and complaint portals; California BPC §17600 et seq. resources via oag.ca.gov; New York AG and consumer pages; DC OAG on the Automatic Renewal Protections Act; Colorado AG resources; Illinois Automatic Contract Renewal Act references; Vermont AGO negative-option pages.

- Payment and platforms: My card issuer's billing error dispute page for deadlines and documentation; the Apple and Google account pages for subscription management and refund requests.

If I need to show how a page looked when I subscribed (not after the seller fixed it), I save copies or use reputable web archives to capture historical versions.

A final note on mindset

I can be fair and firm at the same time. Many subscriptions are legitimate and transparent; some are not. When I ask, "Can I sue a company for auto-renewal subscriptions?" I start with three pillars: were the terms clear before I paid, did I give real consent, and could I cancel without jumping through hoops. If any answer tilts no, I have leverage - in a refund request, a chargeback, or, if needed, in court. I keep my records tight and my timeline tight. That combination often turns a frustrating charge into a clean fix - and sometimes into a broader change that helps the next person too.

.svg)

.svg)

.svg)