Google’s Project Suncatcher raises a practical question for marketers: if Google can shift a chunk of AI compute to solar-powered satellites in low Earth orbit, will model costs, ad product cadence, and SEO dynamics change this decade - or is this a 2030s story?

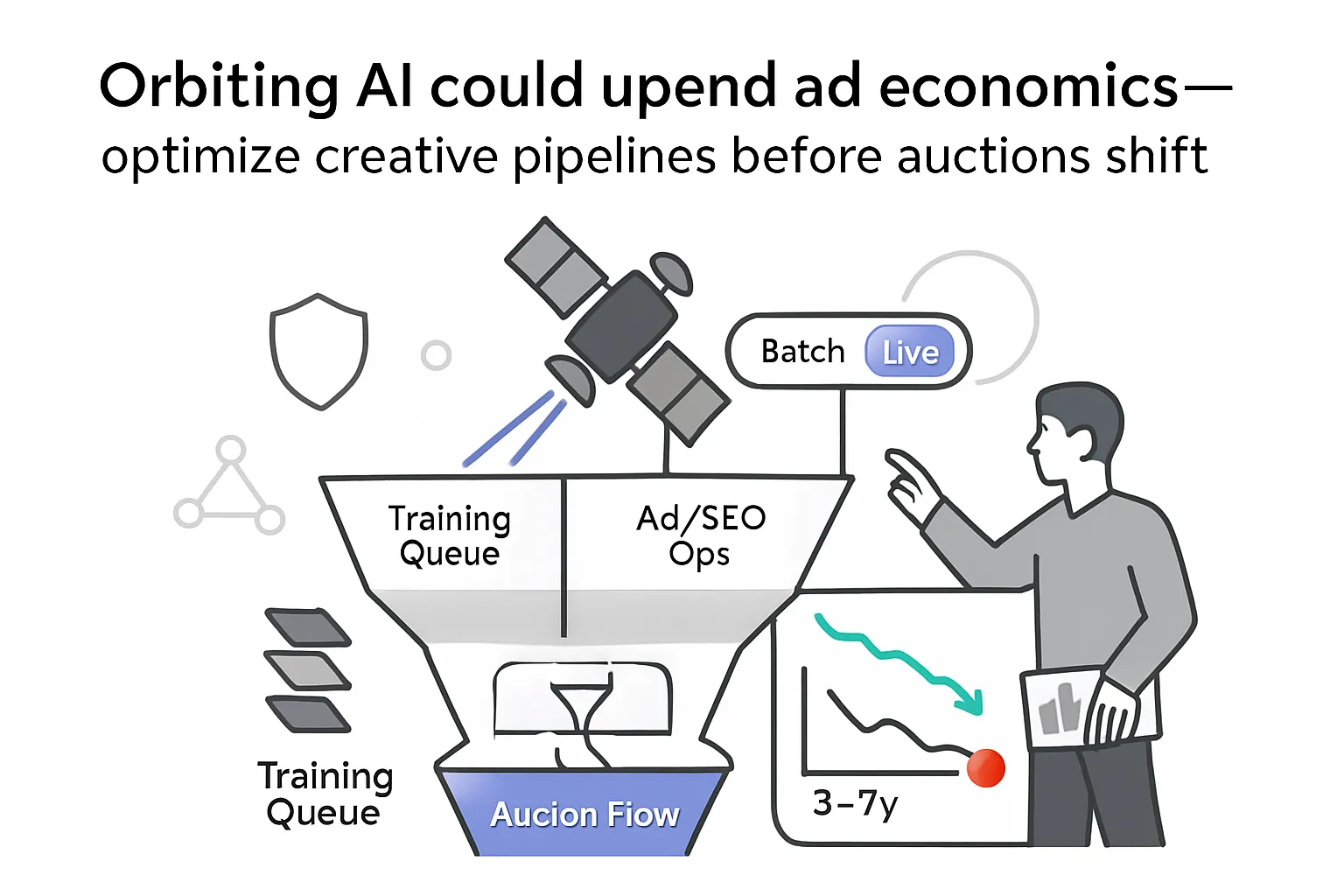

Google Project Suncatcher: how space-based AI compute may cut model costs and shift ad platform features

Thesis: The core claim to evaluate is whether Google’s plan to host Google TPUs on tightly clustered, solar-fed satellites connected by free-space optical links can create enough low-marginal-cost compute to reprice AI models that power ads, search, and creative tooling. The near-term reality is R&D and prototypes; the medium-term effect is cost pressure on training and batch inference, not real-time ad auctions. If launch costs drop toward <$200/kg as Google models, orbital compute could match or undercut the energy component of terrestrial data center costs, increasing supply and bending AI pricing curves. That cost relief would likely appear first in platform features (more generative coverage, richer creative automation) before it shows up as direct media price changes.

Key Takeaways

- Cost curve signal, not an immediate supply shock: If launch costs fall to <$200/kg by the mid‑2030s, Google estimates orbital solar compute can meet terrestrial energy cost levels per kW‑year [S1][S2]. So what: Expect steady AI API price pressure over a 3–7 year window rather than a sudden drop; plan contracts and unit economics around gradual reductions.

- Latency gates use cases: LEO latency is competitive but ground links and capacity make training and batch workloads the first beneficiaries; real-time ad auctions remain ground-based near term [S1][S3]. So what: Anticipate cheaper batch creative generation and model fine-tuning before any change to auction latency or on-page inference.

- Platform advantage accrues to Google: Owning TPUs plus orbital power plus the ads/search stack concentrates gains in Google properties first. So what: Watch Gemini/Ads feature rollout and API pricing; build pricing clauses that pass platform cost reductions through to you.

- SEO exposure likely increases: Cheaper compute enables broader AI overviews and synthesis at the query tail. So what: Prepare for higher zero-click rates where AI answers expand; invest in SERP features that still click (shopping units, video, local packs) and on-site engagement signals.

- Creative throughput expands: Lower marginal compute cost supports more variants and larger video models. So what: Shift creative ops to volume testing (for example, 10–50 variants per concept) with strict brand guardrails and measurable lift targets.

Situation Snapshot

- Trigger: Google Research announced Project Suncatcher, proposing compact LEO constellations with TPUs connected via high-bandwidth optical links, a 2027 two-satellite learning mission with Planet, and a cost model pointing to <$200/kg launches enabling competitive per‑kW‑year economics versus terrestrial energy costs [S1][S2].

- Facts from Google’s post/preprint:

- Bench optical link demo: 800 Gbps each way (1.6 Tbps total) per transceiver pair; goal is tens of Tbps via dense wavelength-division multiplexing and spatial multiplexing in close formations (hundreds of meters) [S1][S2].

- Orbital dynamics modeling shows modest station-keeping for approximately 100–200 m neighbor spacing at ~650 km sun-synchronous orbit [S1][S2].

- TPU v6e (Trillium) radiation tests: High Bandwidth Memory showed irregularities after 2 krad(Si) vs. expected shielded 5-year dose ~0.75 krad(Si); no hard failures up to 15 krad(Si) [S1][S7].

- Economic claim: with sustained launch learning rates, <$200/kg by the mid‑2030s could make orbital compute competitive on a per‑kW‑year basis with data center energy costs [S1][S2].

- Context: LEO systems like Starlink show ~25–40 ms typical latencies to users today [S3], implying practicality for training, fine-tuning, and batch inference but leaving strict real-time ad serving anchored to terrestrial edges.

Breakdown & Mechanics

Energy economics and cost pass-through

Sunlight duty cycle in dawn–dusk sun-synchronous orbits is high; panels in orbit can yield up to ~8× Earth surface output per panel area while avoiding clouds and night cycles [S1]. If launch $/kg trends to <$200 and orbital hardware mass per delivered kW is reasonable (assumption), amortized per‑kW‑year can approximate grid energy opex cited by Google [S1][S2]. Chain: Launch learning curve → lower $/kg → more kW deployed in orbit → lower $/kW‑year → downward pressure on $/FLOP → AI API price pressure → cheaper model-powered ad/search features.

Bandwidth and latency define the workload mix

Desired: tens of Tbps inter-satellite bandwidth to mimic data center fabrics [S1]. Mechanics: received power ∝ 1/r², so flying in tight clusters (r ≈ 0.1–1 km) plus dense wavelength-division multiplexing and spatial multiplexing enables Tbps-class links and makes distributed training feasible. Ground egress is the bottleneck: even with optical downlinks, aggregate ground capacity and station siting will cap real-time delivery. Training, fine-tuning, and batch inference lead; latency-sensitive ad auctions follow (if ever).

Hardware viability in radiation

Proton beam tests suggest TPU v6e (Trillium) tolerates expected LEO doses with shielding; HBM is the weak link but within margin for multi-year missions [S1][S7]. Outcome: hardware replacement cycles and error-correction overhead appear manageable for cluster reliability (assumption based on test margins).

Regulatory and operational incentives

Optical crosslinks avoid spectrum issues in space, though ground links face site, weather, and regulatory constraints [S1][S6]. Incentive alignment: Google controls the TPU stack, ads/search, and cloud. Any marginal $/FLOP savings can compound across product lines, accelerating feature rollout before retail price cuts.

A → B → C summaries

- Close formations plus optical multiplexing → Tbps links → viable distributed training in orbit.

- <$200/kg launch plus high solar duty cycle → per‑kW‑year on par with grid → AI API price pressure 3–7 years out.

- Latency and ground egress limits → batch creative and model training first → ad auction stays terrestrial near term.

Impact Assessment

Paid Search/Shopping

Direction: small near-term effect; medium-term model-driven relevance and quality improvements as compute becomes cheaper. Winners/losers: Google Ads gains capability; advertisers with high-quality feeds and conversion signals benefit from improved matching. Weak signal advertisers see less lift.

- Track Quality Score and RSA asset performance deltas by vertical; if platform-side model upgrades roll out, expect 1–3% CTR/CVR shifts (historical range for model refreshes; assumption).

- Negotiate AI feature pricing floors in contracts (for example, per‑asset generation fees indexed to API rate cards).

Organic Search/Content

Direction: broader AI overviews with cheaper compute increase zero-click exposure at the tail. Winners/losers: strong brands with navigational demand and rich SERP assets (video, product, local) fare better; purely informational publishers lose clicks.

- Measure click deltas for queries with AI answers vs. controls; reallocate content toward formats that still earn engagement (how‑to video, tools, productized insights).

- Mark up content with structured data to qualify for rich results that survive AI summaries.

Creative/Brand

Direction: higher creative throughput, especially video/3D, as batch inference and training costs trend down. Winners/losers: teams with asset pipelines and guardrails can scale variant testing; teams without governance face brand drift risk.

- Set quarterly targets for variant count per concept (for example, 10–50) with pre‑approved styles; run lift tests targeting +3–5% CTR/ROAS improvements (assumption based on typical DCO gains).

- Budget by unit: cost per image, per 15‑sec video, per 1M tokens - review quarterly for price cuts tied to platform updates.

Data/Privacy/Security

Direction: potential for “green compute” claims and new data locality questions if processing spans borders via ground stations.

- Ask vendors where inference and training run (country/region, not orbital position); ensure contracts cover data transfer jurisdictions.

Operations & Procurement

Direction: AI spend mix shifts from inference opex to batch workloads as prices ease.

- Insert price‑down clauses pegged to vendor API lists; require pass‑through of platform‑level cost reductions.

- Build a “model cost bill” per campaign (tokens, images, minutes of video) to expose savings as they arrive.

Scenarios & Probabilities

- Base (Likely): 2027 learning mission succeeds; limited pilot capacity by 2029–2030; launch <$350/kg trending toward <$200/kg by the mid‑2030s [S1][S2]. Net effect: 10–20% AI API price relief over 3–5 years; feature expansion in Google Ads/Search precedes cross‑industry price cuts. Marketing impact: moderate - better tools, modest efficiency gains.

- Upside (Possible): Launch achieves <$150/kg by the early 2030s; multi‑hundreds of MW orbital compute online; optical ground links mature. Net effect: 30–50% drop in effective $/FLOP for batch tasks; LLM video becomes cheap; platform feature velocity accelerates. Marketing impact: large - creative throughput jumps; broader AI summaries in SERPs; lower per‑asset costs.

- Downside (Edge): Debris/regulatory delays; thermal or ground link bottlenecks; costs do not beat terrestrial. Net effect: no material pricing change by 2035. Marketing impact: low - status quo with incremental improvements from terrestrial data centers.

Risks, Unknowns, Limitations

- Launch learning rate may stall; <$200/kg is modeled, not achieved yet [S1][S2]. A slowdown would delay price effects.

- Ground egress is unresolved at the required aggregate bandwidth; weather and siting can cap throughput [S1][S6].

- Thermal management in orbit and long-term reliability could add mass/cost, changing per‑kW economics (unknown).

- Regulatory: debris risk, licensing, cross‑border data flows; any major incident could reverse momentum.

- Latency for strict real-time auctions may remain a blocker; if so, ad serving economics stay terrestrial.

- Falsifiers: if AI API prices do not decline relative to hardware trends across 2027–2032, or if Google cancels or pauses the program, the thesis weakens.

Validation: The analysis states a thesis, maps drivers → mechanics → outcomes, quantifies with cited figures and assumptions, contrasts timelines and beneficiaries, and provides actions by channel with scenarios and risks. If more precise price curves emerge from the preprint, integrate them to tighten the API pricing forecasts.

Sources

- [S1]: Google Research Blog, 2025‑11‑04, announcement - “Exploring a space‑based, scalable AI infrastructure system design (Project Suncatcher)”

- [S2]: Google Research, 2025‑11, preprint - Towards a future space-based, highly scalable AI infrastructure system design

- [S3]: Ookla, 2023‑2024, report - Starlink performance (latency typically ~25–40 ms in U.S.)

- [S4]: U.S. EIA, 2024‑2025, data - Average industrial electricity prices (~$0.08–$0.10/kWh)

- [S5]: International Energy Agency, 2024, briefing - Data centres and data transmission networks outlook

- [S6]: NASA, 2022‑2024, technology notes - Laser Communications Relay and DSOC demonstrations

- [S7]: Google Cloud Blog, 2024‑2025, product note - Trillium (6th‑gen TPU v6e) specs and context

.svg)

.svg)

.svg)